You're trying to help yourself or someone you love. You have an insurance card in one hand, a dozen browser tabs open, and no clear answer to the question that matters most: Will insurance cover the treatment we need?

That moment is more common than people realize. Families in Orange County often reach the same point after a crisis worsens, a therapist recommends a higher level of care, or weekly appointments stop being enough. They know they need more support. What they don't know is how to read the policy, what counts as covered care, or how to get approval for a program like PHP or IOP without spending hours arguing with an insurer.

Insurance coverage for mental health is supposed to make treatment more accessible. Sometimes it does. Sometimes it creates a second layer of stress right when people are least equipped to handle it. The good news is that this process gets easier when you break it into small, concrete steps.

Table of Contents

- The First Step Toward Help Can Feel the Hardest

- Understanding Your Mental Health Insurance Policy

- What Mental Health Services Are Typically Covered

- How to Check Your Benefits and Verify Coverage

- Preauthorization for Higher Levels of Care like PHP and IOP

- Handling Denials and Using Out-of-Network Benefits

- Your Next Steps for Mental Health Care in Orange County

- Frequently Asked Questions About Mental Health Coverage

The First Step Toward Help Can Feel the Hardest

A lot of families freeze at the same exact point. A therapist says, “Your daughter may need something more structured.” A spouse has stopped going to work and barely gets out of bed. An adult son is struggling with anxiety, depression, and drinking, and everyone agrees that once-a-week therapy isn't enough anymore.

Then the practical questions hit all at once.

Do we call the insurance company first? Do we find a program first? Is PHP covered the same way as therapy? What if the website says one thing and the admissions team says another? What if we choose the wrong place and get stuck with a bill we didn't expect?

That confusion isn't a sign that you're doing anything wrong. Insurance language is hard to follow even when you're calm. It gets much harder when you're exhausted, worried, or trying to make decisions quickly.

There's also a real reason to pay attention to coverage. In 2024, adults with insurance were more than twice as likely to receive mental health care as adults without insurance, 25% versus 11%, according to KFF's analysis of mental health care use by demographics and insurance status. The same KFF review notes that having private insurance increases the odds of receiving treatment by over 1.5 times.

That doesn't mean insurance solves everything. It does mean coverage can change what options are available, how quickly a family can move, and whether a higher level of care is financially realistic.

Practical rule: Don't wait to understand every insurance term before you start asking for help. Start the process, then clarify the details as you go.

If you're in Orange County and looking at PHP or IOP, think of this as a working roadmap. You're not trying to become an insurance expert overnight. You're trying to answer a few urgent questions in the right order, avoid common mistakes, and get your loved one into the level of care that fits.

Understanding Your Mental Health Insurance Policy

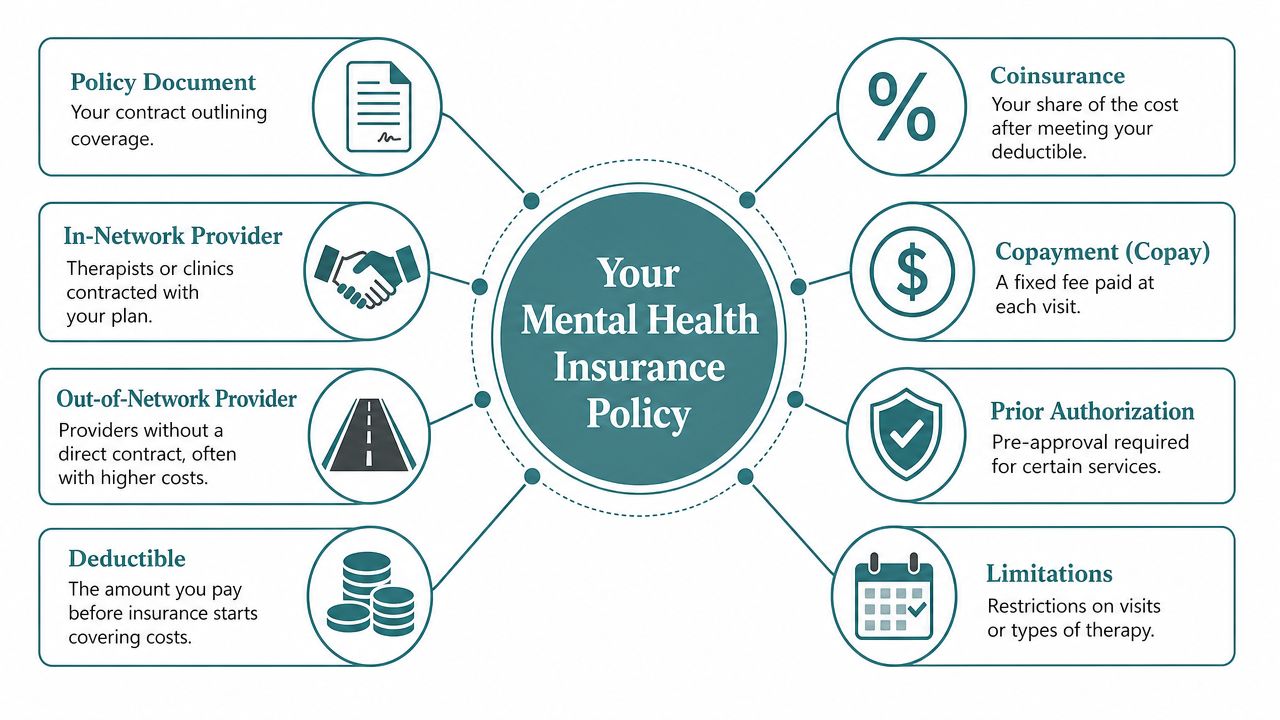

Individuals don't need a perfect understanding of their plan. They need a usable one. The easiest way to get there is to stop reading the policy like a legal contract and start reading it like a payment system with rules.

Start with the money words

Think of your insurance plan like a coffee shop rewards setup.

You pay each month to stay in the program. That's your premium. It doesn't mean everything is free. It means you're enrolled and eligible to use the plan.

Before your insurer starts sharing more of the bill, you may need to pay a set amount yourself. That's your deductible. Some services apply to it. Some don't. Mental health treatment often depends on the exact plan design, so you need to check.

After that, your share may look like one of these:

- Copay means a fixed amount for a visit or service.

- Coinsurance means a percentage of the allowed cost.

- Out-of-pocket maximum is the most you pay for covered services in a plan period before the insurer pays more fully under the terms of the plan.

Two more terms matter a lot when you're looking for mental health care:

| Term | What it usually means for you |

|---|---|

| In-network | The provider has a contract with your plan. Costs are usually lower and billing is often more straightforward. |

| Out-of-network | The provider does not have that contract. Costs may be higher, but some plans still reimburse part of the expense. |

Another phrase that causes stress is prior authorization. That means the insurer wants clinical information before it agrees to cover a service. It doesn't always mean “no.” It means “show us why this level of care is needed.”

If you're trying to understand coverage for a specific diagnosis, this overview of whether insurance covers depression treatment can help you see how policy language often translates into actual treatment access.

Know the rules that protect you

Two laws matter in everyday language, even if they are never read directly.

The Mental Health Parity and Addiction Equity Act says many plans can't make mental health benefits more restrictive than medical or surgical benefits in key ways. The Affordable Care Act also helped make mental health and substance use treatment part of essential coverage requirements for many plans.

In plain terms, that means many insurance plans must cover mental health care, and they're not supposed to treat it like an optional extra while covering physical health more generously.

Still, families get confused because “covered” doesn't always mean simple. A service can be covered but limited by network rules, prior authorization, medical necessity criteria, or documentation requirements.

Coverage answers one question. Access answers another. A plan can list a benefit and still make you work hard to use it.

That gap is why understanding your policy matters so much. Once you know the small set of terms above, the rest of the process gets less mysterious.

What Mental Health Services Are Typically Covered

Insurance coverage for mental health usually depends on level of care. That's the phrase insurers and treatment teams use to describe how intensive the treatment is.

A weekly therapy appointment is one level of care. Psychiatry is another. PHP and IOP sit higher because they involve more structure, more clinical time, and more oversight.

Outpatient therapy

This is often what is pictured first. One session each week with a licensed therapist, in person or by telehealth.

Insurers commonly cover outpatient therapy when the provider is in network and the service is billed under a covered behavioral health benefit. The patient's cost may be a copay, coinsurance, or part of a deductible, depending on the plan.

Coverage questions usually include:

- Provider status: Is the therapist in network or out of network?

- Visit rules: Does the plan require authorization after a certain point?

- Type of therapy: Is the service individual, family, or couples work, and how is it billed?

If your main concern is cost at the standard outpatient level, this guide on how to find affordable therapy can help you compare in-network care, reimbursement options, and practical cost-saving approaches.

Psychiatry and medication management

Psychiatry visits are often covered separately from psychotherapy. A psychiatrist or psychiatric nurse practitioner may evaluate symptoms, prescribe medication, monitor side effects, and adjust treatment over time.

Families often assume medication visits and therapy sessions are processed the same way. They often aren't. Different provider types, billing codes, and network arrangements can affect coverage.

A simple example helps. Someone in Irvine may have a therapist who is out of network but a psychiatrist who is in network through the same insurer. The plan may reimburse those services in completely different ways, even though both are mental health care.

Higher levels of care

PHP and IOP are where the insurance conversation usually gets more detailed.

Intensive Outpatient Program (IOP) is typically used when someone needs more support than weekly therapy but doesn't require inpatient hospitalization. It usually includes multiple treatment sessions each week, group work, individual therapy, and sometimes psychiatric support.

Partial Hospitalization Program (PHP) is more intensive. It usually involves structured, full-day treatment while the person still lives at home or in supportive housing.

Insurers evaluate PHP and IOP differently because these aren't one-off visits. They are organized programs with a treatment schedule, clinical goals, and ongoing review. The insurer will usually want to know why a lower level of care is not enough and why inpatient care is not the better fit.

The closer a service gets to daily structured treatment, the more likely the insurer is to ask for clinical justification before approving it.

That's why a family may find that weekly therapy was easy to start, while PHP approval requires records, intake assessments, and utilization review. It's not necessarily a sign that coverage doesn't exist. It usually means the insurer is applying a different review process.

How to Check Your Benefits and Verify Coverage

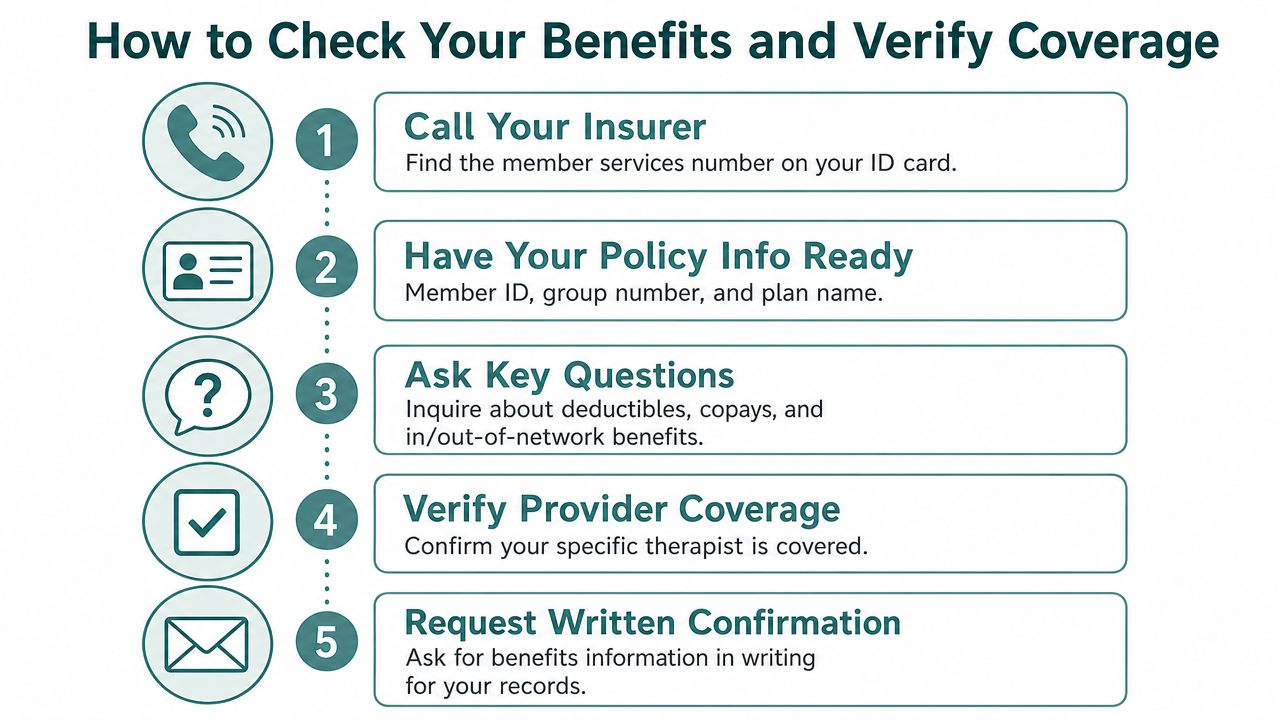

This is the part that gives families the most relief once they know how to do it. Don't rely on one source alone. Verify your benefits in more than one way, then compare what you hear.

Call the number on your card

Start with the member services number on the back of the insurance card. When you call, have the policyholder's full name, member ID, group number, and date of birth ready.

Then slow the conversation down and ask direct questions. Write down the representative's name, the date, and any reference number for the call. If your family has records spread across phones, emails, and paper folders, using an organized system like a Family Folder for family medical records can make these conversations much easier to track.

Ask questions like these:

- Does my plan include behavioral health benefits for outpatient mental health treatment?

- Do I have in-network and out-of-network benefits for mental health care?

- What is my deductible, and has any of it been met?

- What are my copay or coinsurance responsibilities for therapy, psychiatry, IOP, and PHP?

- Does PHP or IOP require prior authorization or preauthorization?

- Are there any exclusions, visit limits, or medical necessity requirements I should know about?

- If I use an out-of-network provider, how do I submit claims and what paperwork is required?

- Can you send this benefits information in writing through the member portal or by email?

Ask the insurer to explain your benefits for the exact level of care you're considering. “Mental health coverage” is too broad to be useful on its own.

Use the member portal

Most insurers now give members online access to plan documents, claims, deductibles, and provider directories. This can help you confirm basic cost-sharing rules without waiting on hold.

Use the portal to check three things in particular:

- Benefit summaries for behavioral health services

- Provider search tools for psychiatrists, therapists, and treatment programs

- Claims history to see whether deductibles have already been applied this year

Be cautious with directories. They're helpful, but they aren't always current. A listing can show a provider as in network even when they're no longer accepting new patients or no longer working at that location.

Ask the treatment center to verify benefits

The most practical step for PHP or IOP is often a Verification of Benefits, commonly called a VOB. That means the admissions team contacts the insurer, confirms the plan details, and checks how the benefits may apply to the program you're considering.

If you're exploring a higher level of care, you can request insurance verification through Casa Recovery admissions as one example of this process. A VOB doesn't replace final authorization from the insurer, but it usually gives families a much clearer picture of network status, expected responsibility, and whether preauthorization will be needed.

A strong VOB call usually confirms:

| What to verify | Why it matters |

|---|---|

| Plan type | PPO, employer plan, behavioral health carve-out, or another structure can change how claims are handled |

| Network status | This affects cost and whether single-case or reimbursement options are relevant |

| Authorization needs | PHP and IOP often require additional review before treatment starts |

| Financial estimate | Families need a reasonable expectation of what they may owe |

When a family is under pressure, this step often saves time and reduces confusion. Instead of trying to translate policy language alone, they can compare insurer information with provider-side verification and make decisions from there.

Preauthorization for Higher Levels of Care like PHP and IOP

Families often hear two phrases during admissions calls that sound similar but mean different things: medical necessity and preauthorization.

Medical necessity is the clinical reason the treatment is needed. Preauthorization is the insurer's review process for deciding whether it will approve coverage for that treatment.

What medical necessity means

For PHP or IOP, the treatment provider usually gathers clinical information during the assessment. That may include current symptoms, safety concerns, recent functioning, failed lower levels of care, medication issues, family concerns, and whether the person can manage daily life without more support.

The provider then uses that information to explain why the recommended level of care fits the patient's current needs. If you're still trying to sort out which program makes sense, this comparison of how IOP is different than PHP can make the distinction easier to understand before insurance review begins.

A simple way to view this:

- Medical necessity asks: Why does this person need this level of care now?

- Preauthorization asks: Will the insurer approve coverage based on the information provided?

When the clinical picture is clear and well documented, the provider has a stronger case to present.

Why approval can still be difficult

Many families feel blindsided. Even with insurance, easy access is not guaranteed.

According to a 2021 report discussed by Strengthen Healthcare on the mental health coverage gap, roughly two-thirds of Americans with diagnosed mental health conditions were unable to access treatment despite having insurance, often because of claim denials and arbitrary medical necessity standards. The same report notes that behavioral health reimbursement rates are, on average, 22% lower than for medical visits, which can discourage providers from joining insurer networks.

That helps explain why families run into problems such as:

- Narrow networks: The plan technically offers coverage, but there may be few available providers for the needed level of care.

- Strict review standards: The insurer may say outpatient care should be tried first, even when the family and clinician feel that isn't enough.

- Ongoing authorization checks: Approval may need to be renewed as treatment continues.

Some of the hardest insurance problems aren't about whether mental health care exists as a benefit. They're about whether the insurer agrees with the level, timing, or provider.

That's why PHP and IOP admissions often involve both clinical and administrative work at the same time. The family is deciding what's needed. The provider is documenting why. The insurer is reviewing whether it agrees.

Handling Denials and Using Out-of-Network Benefits

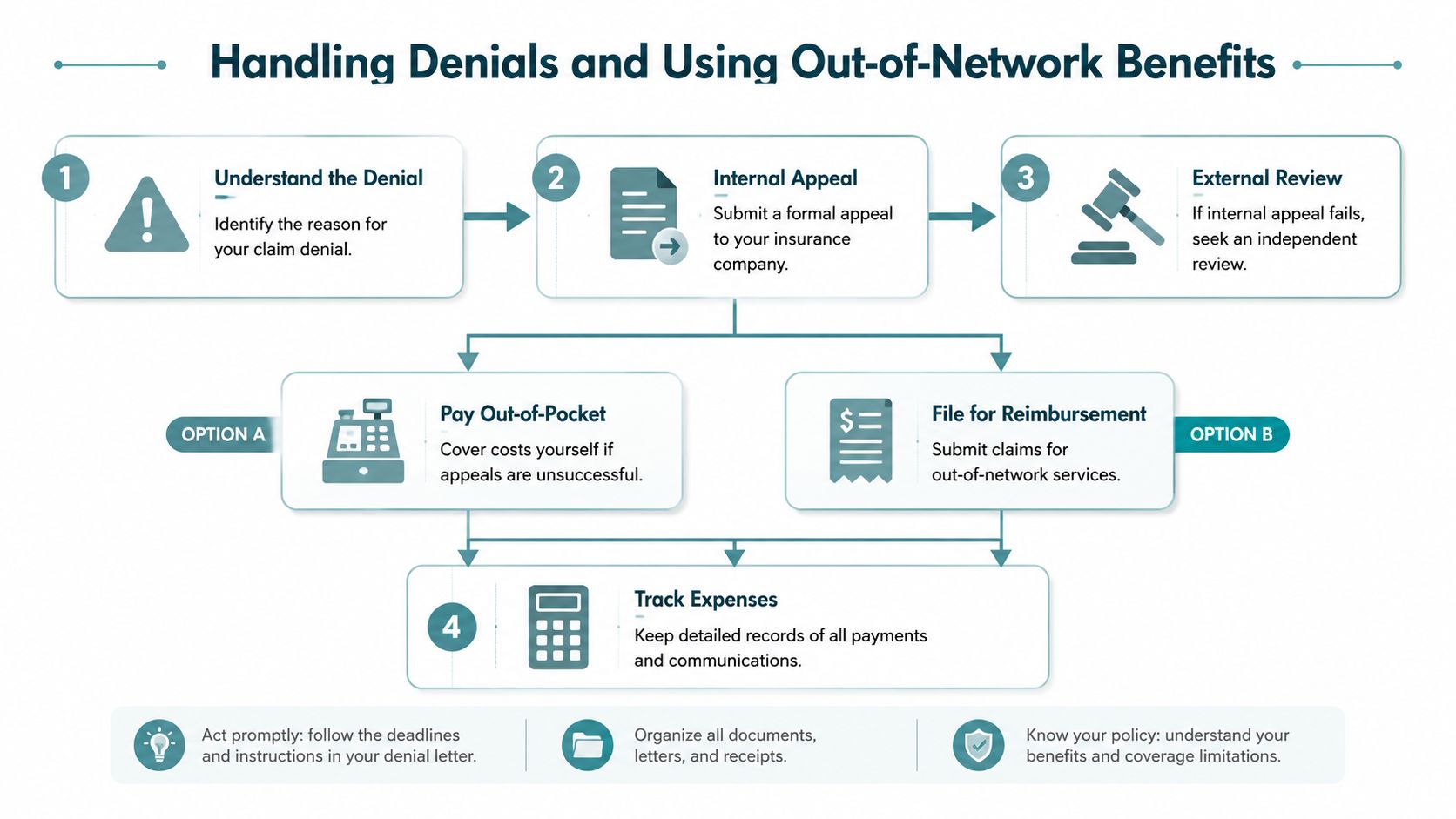

A denial feels personal when you're already stretched thin. It helps to treat it as an insurance event, not as a judgment about whether treatment is needed.

A denial is a process point, not the end

Read the denial letter carefully. Insurers usually state a reason, even if the wording is frustratingly technical. Common themes include lack of authorization, questions about medical necessity, incomplete documentation, or network issues.

From there, the next steps usually look like this:

- Request the exact reason in writing. Don't rely on a phone summary if the written notice says something different.

- File an internal appeal. This asks the insurer to reconsider based on additional records, clinical notes, or a more detailed explanation from the provider.

- Pursue external review if available. That means an independent party reviews the denial after the insurer's internal process is exhausted.

Keep records of every call, fax, portal message, and letter. If your provider needs to send records quickly and securely, a practical walkthrough like this SendItFax guide on secure medical transmissions can help families understand how medical documents are commonly transmitted and tracked.

When out-of-network benefits make sense

Many people assume out-of-network care means paying everything yourself. That isn't always true.

If you have a PPO plan with out-of-network benefits, you may be able to receive care from a provider outside the insurer's contracted network and then seek partial reimbursement. The provider may give you a superbill, which is an itemized statement you can submit to the insurer.

This option can matter when:

| Situation | Why out-of-network may help |

|---|---|

| No suitable in-network program is available | The family may need to move forward with the provider that can actually admit the patient |

| The needed specialty is hard to find | Trauma-focused care, dual diagnosis support, or a specific program format may not be easy to locate in network |

| The network provider wait is too long | Delaying care can create more risk and more disruption |

You'll want to ask very specific questions before choosing this route:

- What is the out-of-network deductible?

- What percentage of the allowed amount will the plan reimburse?

- Does the provider bill the insurer directly, or does the family pay first and submit claims?

- Will the insurer accept a superbill for this level of care?

Sometimes the best choice is not the cheapest one on paper. It's the one that gets the right treatment started without unnecessary delay, while keeping as much reimbursement on the table as possible.

Your Next Steps for Mental Health Care in Orange County

If you're in Orange County, the most useful next move is usually not “research more.” It's to gather the right information and start the verification process with a provider that offers the level of care being considered.

What to have ready before you call

Keep this short list in front of you:

- Insurance card details: Member ID, group number, and policyholder information

- Clinical context: Recent symptoms, current providers, medications, and any recommendation for PHP or IOP

- Logistics: Where the person lives, whether transportation is manageable, and whether they need daytime structure or a step-down schedule

- Questions: In-network status, PPO use, preauthorization needs, psychiatry access, and family involvement

That preparation helps the admissions conversation stay focused. It also helps the treatment team identify coverage issues early, before a family commits to a plan they don't fully understand.

A local option for PHP and IOP

For families seeking structured outpatient mental health care in San Juan Capistrano and the broader Orange County area, Casa Recovery offers PHP, IOP, mental health treatment, dual-diagnosis care, psychiatric services, individual therapy, group therapy, and family programming. According to the publisher information provided for this article, the center works with all PPO plans and is in network with Blue Shield of California and Blue Card, ComPsych, and Holman Group.

For many families, the practical value is that an admissions team can help handle the insurance side of the process. That can include benefit verification, checking network status, identifying preauthorization requirements, and clarifying what information the insurer may need before treatment begins.

If you're trying to make a decision quickly, that kind of support can remove a major source of delay. Instead of guessing what your plan means, you can start with your actual policy details and a real assessment of what level of care may fit.

Frequently Asked Questions About Mental Health Coverage

Does insurance cover family or couples therapy

Sometimes, but it depends on how the service is billed and why it's being provided. Many plans are more likely to cover family sessions when they are part of treatment for an identified patient with a covered mental health diagnosis. Couples therapy is more variable. If the focus is relationship support rather than treatment of a diagnosed condition, coverage may be limited or excluded.

What if I don't have health insurance

Start by asking providers whether they offer self-pay options, payment plans, or lower-cost outpatient alternatives. Community mental health clinics, county behavioral health programs, and nonprofit resources may also help. If someone needs a higher level of care, ask the admissions team what uninsured pathways exist instead of assuming treatment is out of reach.

Is dual diagnosis treatment covered

It often can be, especially when the plan includes behavioral health and substance use disorder benefits. Coverage still depends on the level of care, medical necessity review, and provider arrangement with the insurer. The key is to ask whether the program can treat both conditions together rather than sending you to separate services.

If you're weighing treatment options and need help sorting out insurance coverage for mental health, Casa Recovery can help you take the next step. Their admissions team can review your policy information, explain how benefits may apply to PHP or IOP, and help your family understand what to expect before treatment starts.